Our latest survey confirms that the future will belong to companies that put technology at the center of their outlook, capabilities, and leadership mandate.

One year into the COVID-19 crisis, our newest McKinsey Global Survey on digital strategy1 indicates that the pandemic has increased the pace of business and that technology capabilities will be critical to companies’ COVID-19 exit strategies as well as to what comes next. After seeing how the pandemic had sped up the adoption of digital technologies by several years, we took a closer look at how companies are rethinking the role of digital technology in their overall business strategy and how to conduct business at the quickening pace that’s now needed to operate.

The imperative for a strategic approach to technology is universal, yet some companies are already leading the pack; their responses show that better overall technology capabilities, talent, leadership, and resources (what we call a company’s “technology endowment”) are linked to better economic outcomes. At the same time, the results confirm that many organizations could be missing opportunities to invest in the areas of their business models that are most at risk of digital disruption.

The pandemic has dramatically increased the speed at which digital is fundamentally changing business

Our previous survey showed that across key areas of the business model, companies’ overall adoption of digital technologies had sped up by three to seven years in a span of months. The newest results show that this acceleration is also happening at the level of core business practices: what was considered best-in-class speed for most business practices in 2018 is now slower than average. And at companies with the strongest technology endowments,2 respondents say they are operating at an even faster pace.

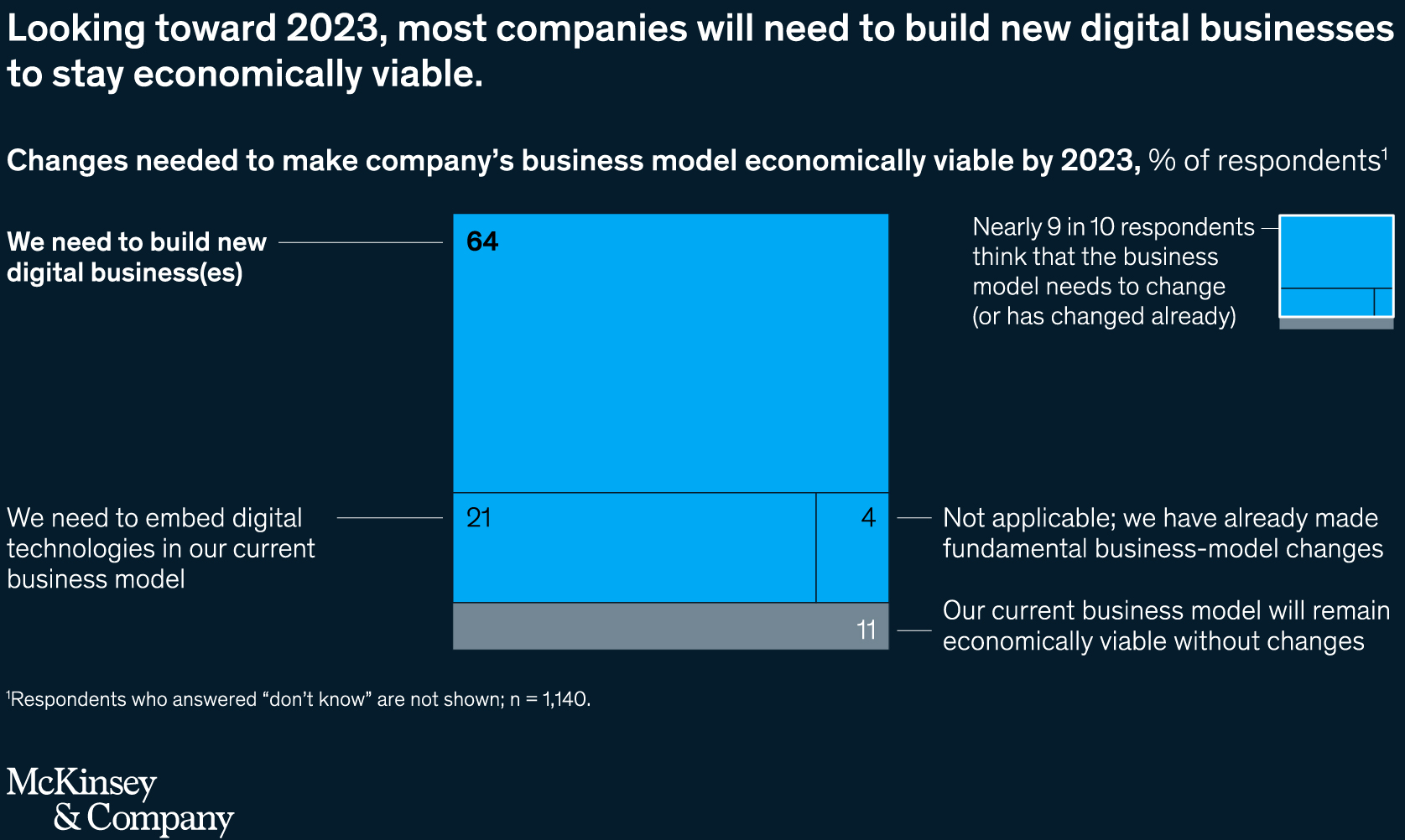

But it’s not only the pace of business that the COVID-19 crisis has fundamentally changed. According to the survey, many respondents recognize that their companies’ business models are becoming obsolete. Only 11 percent believe their current business models will be economically viable through 2023, while another 64 percent say their companies need to build new digital businesses to help them get there.

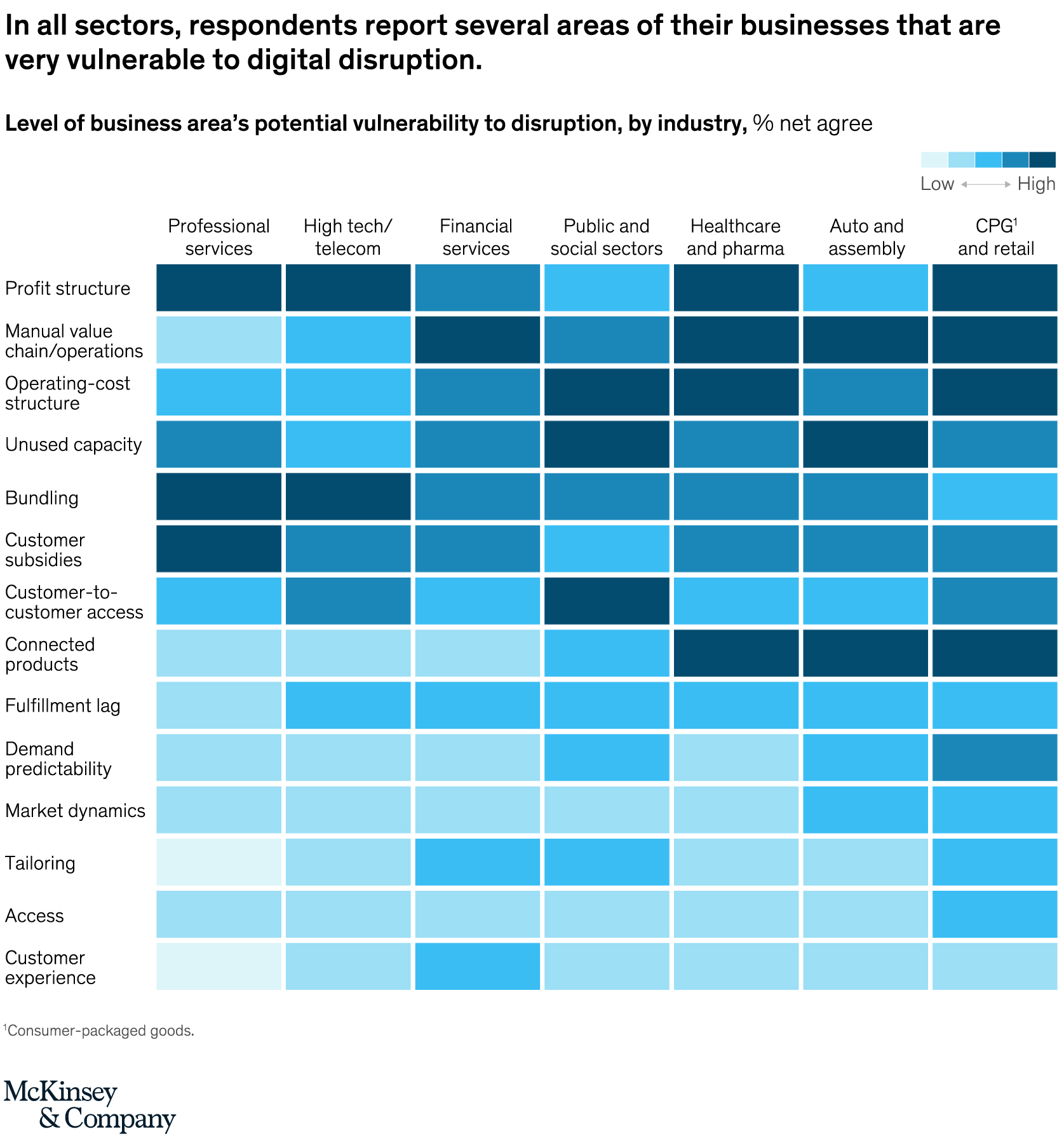

At the same time, the pandemic has created new vulnerabilities to—along with new opportunities from—future disruptions. We know from experience that customers, employees, and value-chain partners have all increased their use of technology, which has made the barriers to digital disruption even lower than before the crisis and paved the way for more rapid, technology-driven changes going forward. In our survey, respondents in every sector say their companies have significant vulnerabilities, especially to their profit structures, ability to bundle products, and operations.

We also looked at the areas of their business where industries have been investing and, for the most part, those investments don’t align with the areas that are most prone to disruption (or that offer the highest returns). For example, many healthcare and pharma companies are investing in tailoring their offerings, enabling on-demand access to products and services, and improving overall customer experience. Yet, according to the survey, these businesses face greater risks of disruption in their value chains, the structure of their operating costs, and the types of products they offer.

To meet new demands, companies are making digital and technology investments across the business model

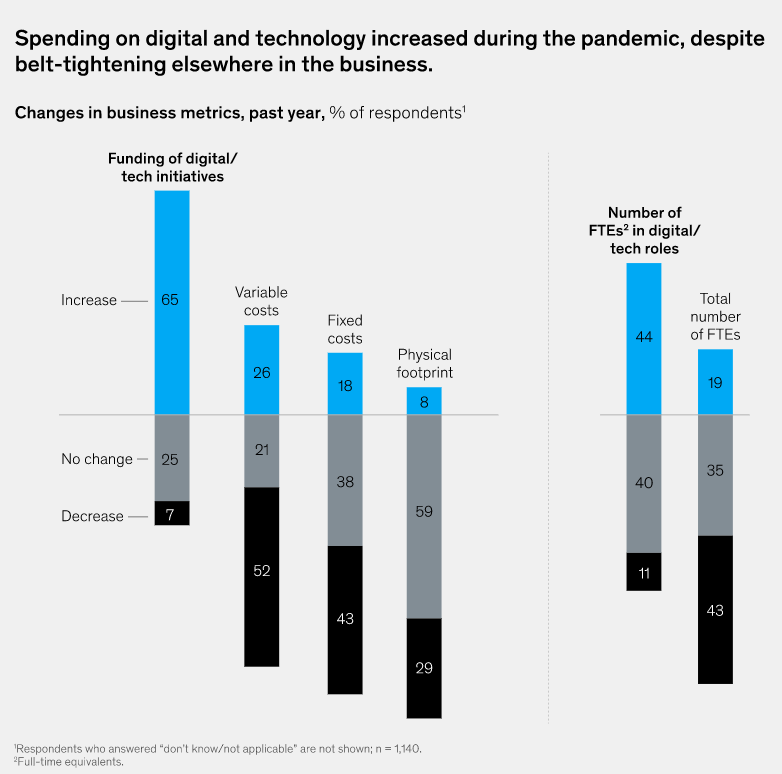

One marker of technology’s increasing importance to both strategy and operations is that companies devoted more resources to their digital and technology capabilities during the pandemic, even as they cut resources from other parts of the business. According to the survey results, the funding of digital and technology initiatives increased, as did the numbers of full-time equivalents in digital and technology roles.

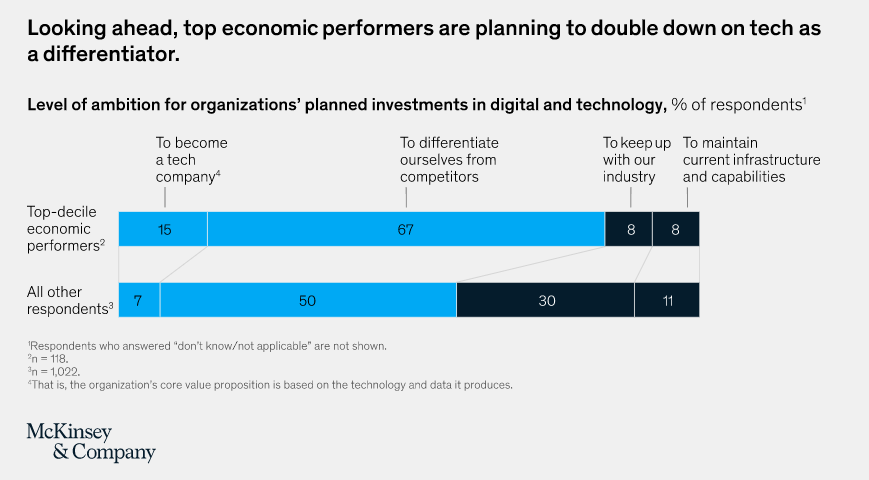

Consistent with last year’s findings that executives have started to take a more strategic view of technology, thinking of it as more than a mere cost driver, more than half of this year’s respondents say their companies are looking to technology as a way to strategically differentiate themselves from competitors.

The highest-performing companies made bolder investments in technology and possess stronger overall capabilities

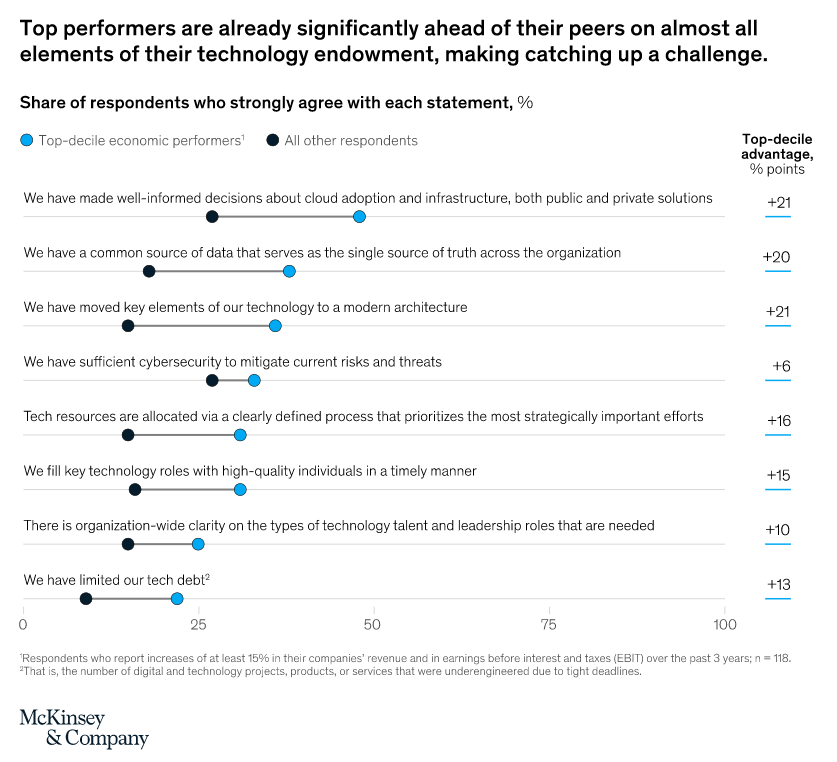

We know from past research that bolder, at-scale investments in technology are significantly more likely to support a successful transformation than those that are smaller in scope. To achieve their ambitions, it’s critical that organizations understand what it really means to differentiate from others on their technology—especially since “technology” and “digital” are such broad terms and mean different things at different organizations. So we asked respondents about specific elements of technology that, based on our experience and prior research, underpin successful digital transformations and make up a company’s technology endowment. The results suggest a clear link between the technology endowment and economic outperformance. When looking at the technology endowment’s individual capabilities (the survey asked about 13 in total), the top-decile economic performers are already significantly ahead of their peers on nearly every one.3 For example, these respondents are nearly twice as likely as others to say they fill key technology roles with high-quality talent in a timely manner. At the same time, the results confirm that even the top performers have room to improve and strengthen their tech endowments.

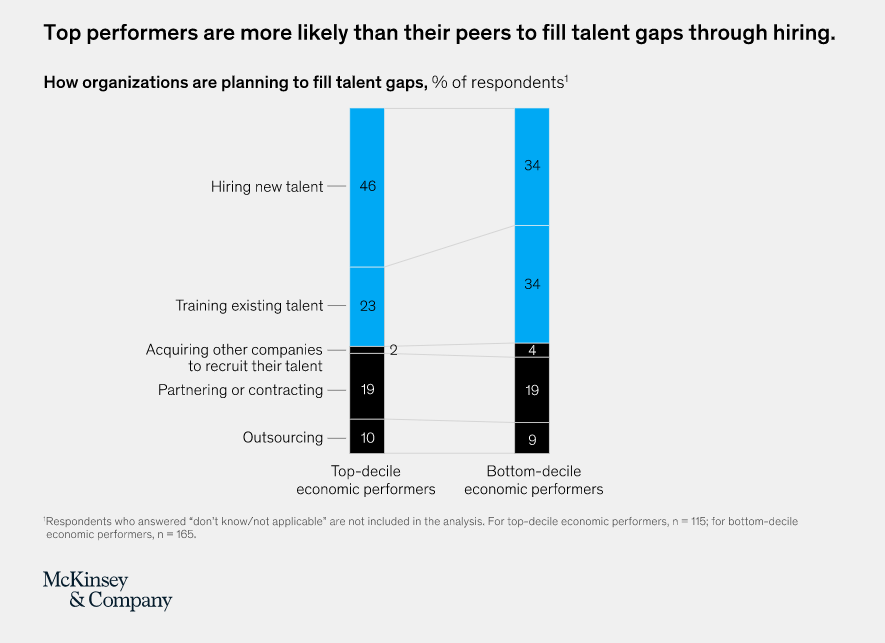

Talent poses a perennial challenge to companies that are transforming their business through digital and technology—as many of our respondents say their companies aim to do. As organizations make their plans for filling critical talent gaps in technology, from the board to the front line, the results suggest that there is no silver bullet to filling skill gaps. Top economic performers report a greater reliance in hiring new employees. At other companies, respondents report an equal focus on hiring and retraining their current people, and the two groups rely equally on partnering or contracting.

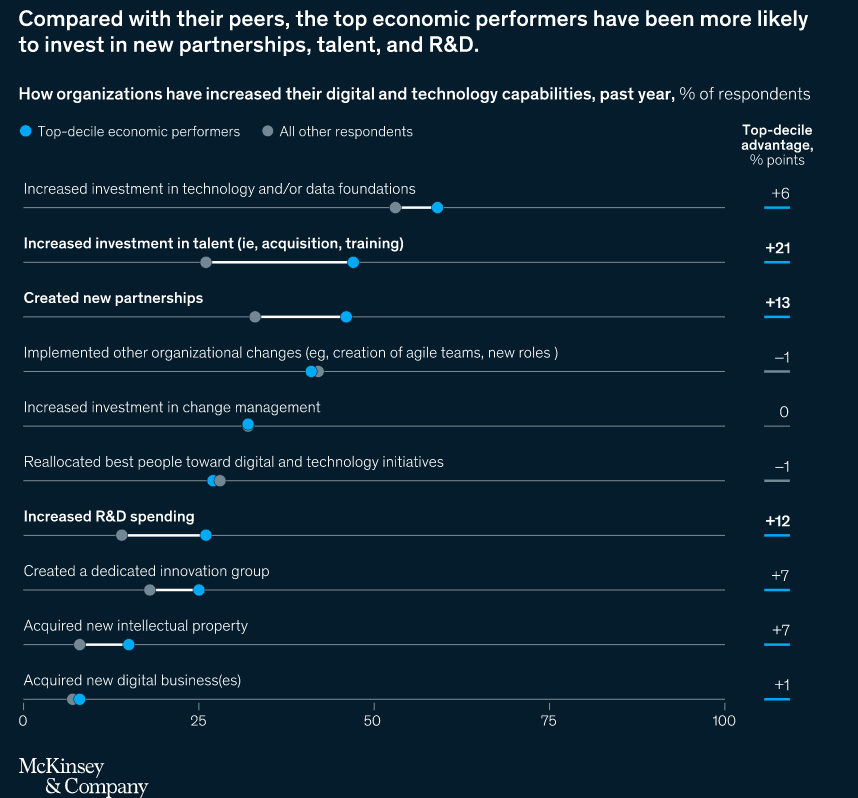

Catching up with the leaders (much less surpassing them) will be increasingly difficult, for the top economic performers have already taken more actions than peers to achieve their technology objectives. Their responses show that these organizations are more likely to invest in talent, create new partnerships (including with competitors), and increase their R&D spending.

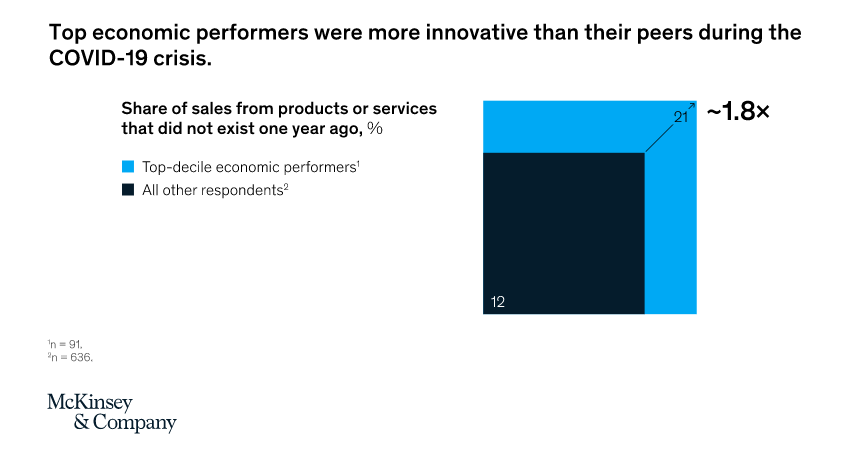

Top-decile performers have also taken a bolder approach to innovation and now obtain a much larger share of their sales from products or services that didn’t exist one year ago.

What’s more, the top-decile performers are making more aggressive plans to differentiate themselves with technology, with some preparing to reinvent their value proposition altogether.

Tech-savvy leadership helped set top performers apart—and will be even more valuable in the future

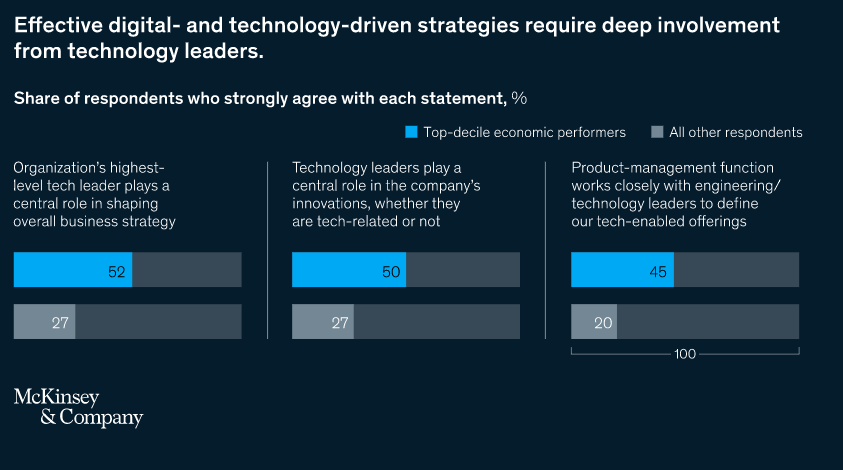

Given technology’s growing importance to business success, it’s perhaps not surprising that top performers are nearly twice as likely to have technology leaders who actively shape overall strategy. They’re also more likely to give tech leaders a major role in innovation and product development.

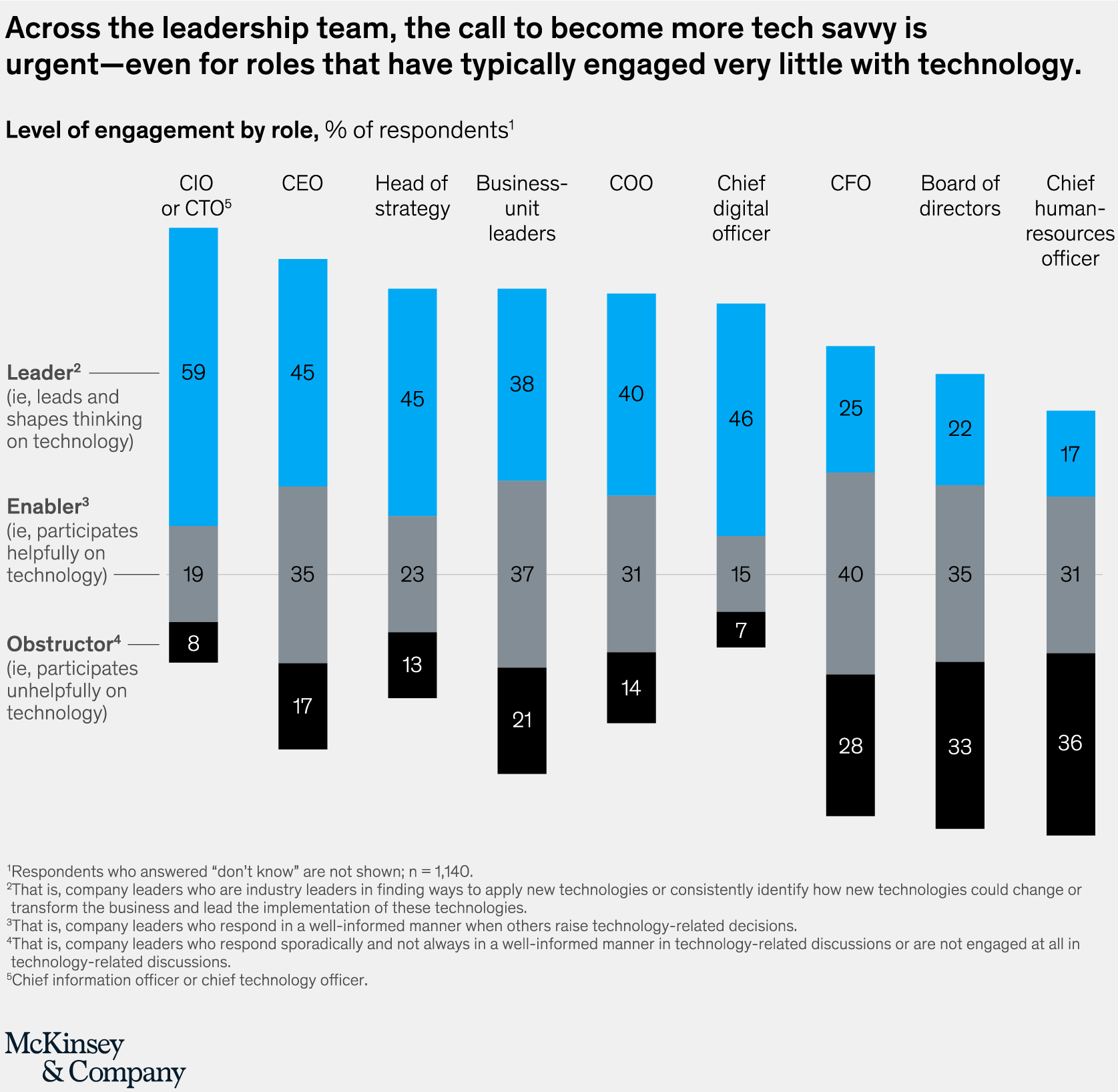

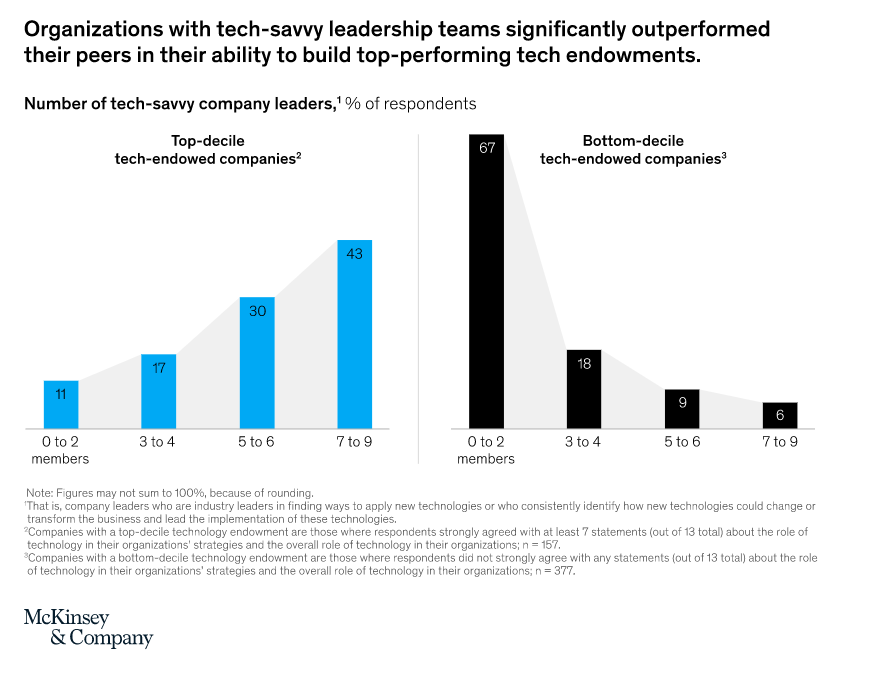

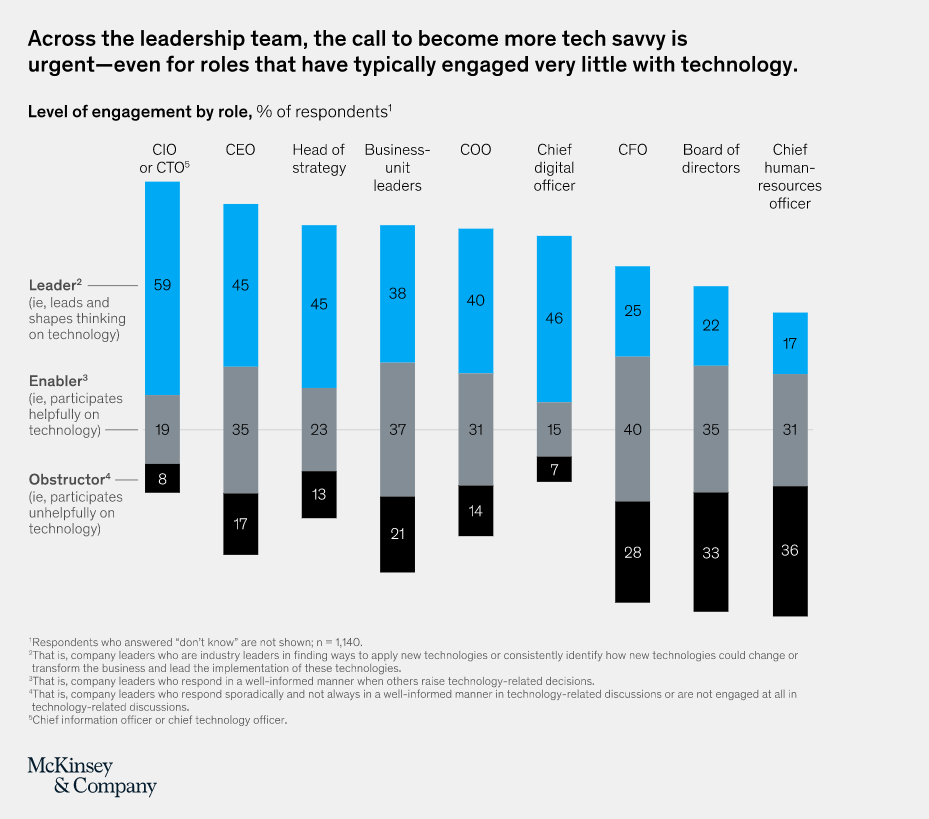

Despite the importance of involving technology leaders in business decisions, it isn’t sufficient for companies to have a single technology leader responsible for driving a top-performing and digitally enabled business strategy. We asked how boards of directors, C-suite leaders, and business-unit heads are engaging in technology. Respondents at the top economic performers are nearly 2.5 times likelier than bottom-decile companies to say seven or more of these roles are leading the technology-related thinking for their organizations. There are even bigger differences at organizations with a top-decile technology endowment: those respondents are more than seven times likelier than the bottom decile to report at least seven tech-savvy leaders.

The importance of digital poses a challenge for company leaders: few are used to engaging with technology, even as it is transforming the requirements of nearly every role and becoming part of everyone’s job. Boards are being asked to communicate to the market about their organization’s investments in digital technologies and how that will enable them to keep pace with competitors. Chief human-resources officers need to not only hire new types of talent but also address questions about artificial intelligence’s role in changing the types and numbers of people their business requires. CFOs need to make larger and faster decisions on investments in digital technologies and, in many cases, spearhead the acquisition of digital companies. Yet according to the survey, the majority of current leaders lack the knowledge or experience to pioneer ways to apply new technologies or consistently identify how new technologies can transform their business. They need to become technology “leaders”—rather than “enablers”4 or “obstructors”5—at their respective organizations.

Looking ahead

The corporate recovery from the COVID-19 crisis will involve permanent changes to many dimensions of an organization: the pace at which it conducts its business, the very nature of that business’s value proposition, and the talent, capabilities, and leadership that are necessary for success. With digital and technology-driven disruptions creating winner-takes-all dynamics in more and more industries, only a small subset of organizations is likely to thrive—and even these companies have much more room to strengthen their technology endowments. Our survey results confirm not only that a strong technology foundation is critical but also that leading companies are far ahead of competitors in building theirs. For everyone else, the time is now to make bold investments in technology and capabilities that will equip their businesses to outperform others in a rapidly evolving landscape .

The time is now for companies to make bold investments in technology and capabilities that will equip their businesses to outperform others.

…

This article first appeared in www.mckinsey.com

Seeking to build and grow your brand using the force of consumer insight, strategic foresight, creative disruption and technology prowess? Talk to us at +971 50 6254340 or mail: engage@groupisd.com or visit www.groupisd.com/story