Companies across the used-car market’s value chain can use data and analytics to tap into growth opportunities and improve margins.

The institutional retail used-car market in the United States and Europe is projected to bring in nearly $1.2 trillion in revenue in 2023. Across both regions, this market is quite fragmented: the top 20 used-car retailers have less than 20 percent market share in America and less than 10 percent in Europe. Compared with other retail segments, this historic fragmentation has led to slow adoption of innovative digital and analytics capabilities across the value chain. It has also opened opportunities for digital-first entrants, elevating pressure on incumbents to innovate.

Moreover, as used-car companies emerge from complicated market dynamics caused by the pandemic, they have been thrust into a new and complex environment, contending with changing consumer preferences, evolving supply-and-demand dynamics, and economic pressures. These influences will make it more difficult for players across the used-car ecosystem to grow and will increase pressure to maintain elevated margins from the pandemic period.

To tap into customer demand, protect margins, and improve performance, companies across the used-car value chain—namely B2B and B2C dealers, OEMs, and financing and leasing companies—must reinvent and redesign business approaches to be more analytically savvy if they want to stay ahead of the competition.

State of the used-car market

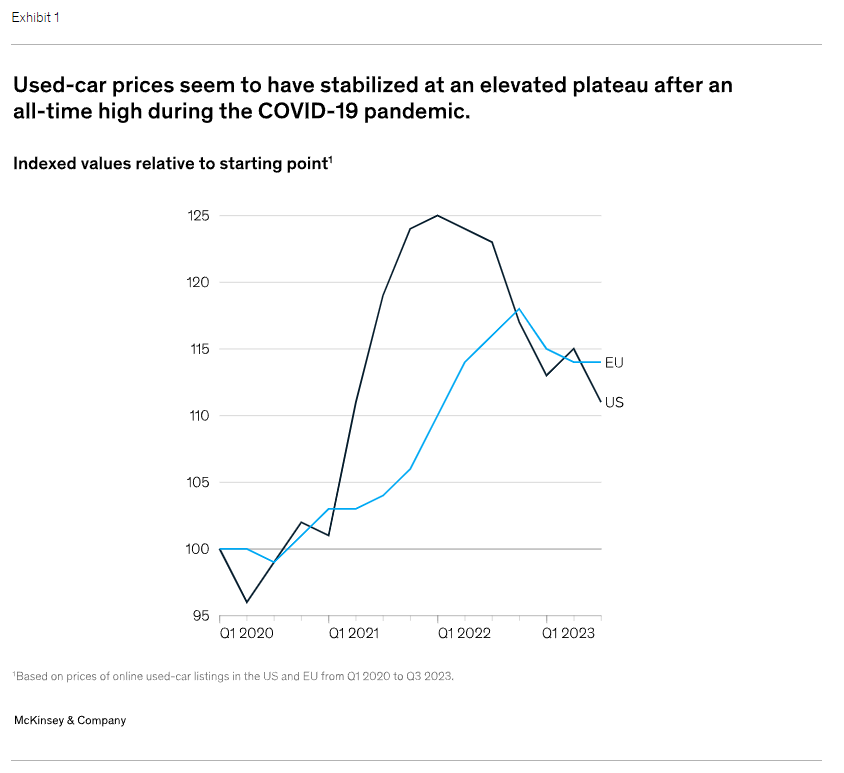

Geopolitical issues and supply chain challenges—specifically the shortage of chips1 and other electronic components—have hampered the supply of both new and used cars over the past several years. This state of strained supply and high demand have allowed for inflated pricing of new and used vehicles and higher margins on sales. Though supply is recovering for some models, demand is now under pressure because of purchasing power depressions driven by inflationary tendencies in many regions. Consequently, dealers are losing some of that pricing power: the average price of a used car in the United States increased by 25 percent between 2020 and its peak in 2022, but it has since fallen (Exhibit 1). Demand and supply are further affected by disruptions in fiscal policy in both markets: higher interest rates increase the cost of financing, which decreases auto finance companies’ margins while also pricing some prospective consumers out of the market. This is especially the case with electric vehicles (EVs) because higher energy prices, the fear of unstable residual values, and the adjustment of subsidies in some markets are jeopardizing the promise of lower total costs of ownership that EVs have made to private retail customers.

Meanwhile, customers continue to shift more of their car-purchasing journey online. According to McKinsey research, more than 95 percent of used-car searches start online with customers researching vehicle information, and more than 70 percent of consumers use third-party websites to compare prices.

Digital-forward companies have tapped into these preferences, evidenced by the rise of used-car marketplaces with value-added services, seamless omnichannel options, and digital financing. These companies allow customers to browse a wide selection of used cars and review and compare pricing. These companies then provide nationwide delivery, relying on algorithm-based decision making for all back-end processes.

How data and analytics can capture value

Currently, many companies across the automotive value chain fail to leverage data to optimize business processes in an exhaustive way and still rely on internal experts and gut feeling for many critical decision-making processes. Adopting data-based decision making could allow dealers, OEMs, and auto finance companies to tap into customer demand, increase margins, and improve performance.

Over the past 20 years, real-time automotive retail has become abundantly available, meaning that pricing should be set as dynamically as it is for airline tickets; long-term assortment decisions should be curated based on customer demand, as they are in consumer retail; and throughput management should be as dynamically managed as it is in manufacturing.

To capture the value associated with analytics along the value chain, used-car companies can take four steps. First, they can combine external data with internal data to create a centralized bank of proprietary data to help stay abreast of market trends and customer needs while maintaining a strategic competitive advantage. Second, rather than deploying generic tools or solutions that are available on the market, they can develop proprietary algorithms that reflect their specific business reality. Third, they can embed analytics-based decision making across all levels of the organization, rather than isolating it to individual applications. Last, they can adjust their governance and operating models to centralize core functions, enabling frontline employees to focus on customer needs. The following section outlines how different players in the ecosystem can employ these steps and the results of doing so.

Dealers

Digitalization can help dealers to pivot to a more sustainable business model—specifically, data-driven analytics can help them determine optimal sourcing and pricing strategies, as well as vehicle allocation, to cater to customer preferences. Dealers can leverage data and analytics in three ways to increase value.

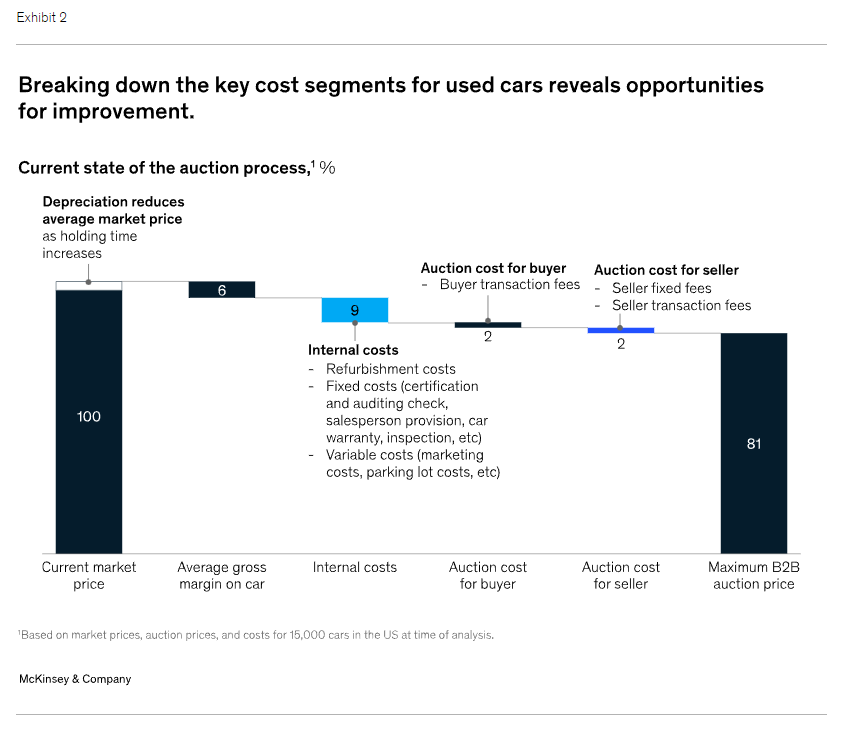

Sourcing and bidding strategy. Dealers can use data on current market inventory to optimize bidding prices and maximize margins. Analytically driven sourcing and bidding models that leverage real-time market data can help dealers determine the desirability of a car across price levels and help determine the optimal bidding price while reducing internal costs.

Exhibit 2 shows the current state of the auction process, which has an average margin of about 6 percent. An assessment of 15,000 car transactions in 2022 and 2023 identified an incremental 2 percent margin-expansion opportunity using dynamic bidding strategies that leverage real-time used-car-market pricing data, translating into a $22 billion opportunity collectively in the United States and Europe.

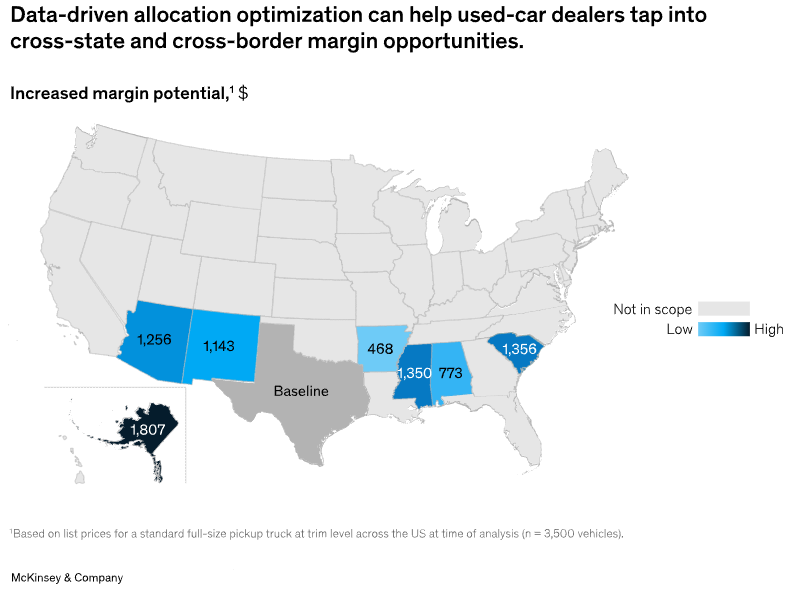

ehicle allocation. Large national dealers can use their economies of scale to leverage differences in regional pricing to improve margins. Dealers can use real-time market demand and pricing data to allocate individual vehicles within a dealership’s network based on the best regional market price (net of shipping costs) and holding periods to maximize margins.

Exhibit 3 shows an example of the price differential (net of shipping costs) for a specific trim line of a full-size pickup truck across states. In this example, a national dealer based in Texas can leverage this real-time market data to extract higher margins by selling the car in Arizona, New Mexico, Arkansas, Alabama, or South Carolina instead of its base state.Exhibit 3

Based on cross-border potential and margin increases per vehicle, the annual opportunity from analytically enhanced vehicle-allocation strategies is collectively $1.2 billion in the United States and Europe.

Decision making and frontline sales performance. Dealers can embed real-time market data to assess and improve local branch and market performances. For example, dealers could optimize their pricing and inventory based on local market trends and inventory levels in a designated market area. Distributed dealerships could then enable field sales teams to make data-backed decisions in their day-to-day roles to improve performance.

OEMs

Gathering real-time feedback from the market on car value performance can be challenging for OEMs, and it can be difficult to know how vehicles are performing after they’re on the market for a few years. Understanding vehicle performance in terms of value in the used-car space can help OEMs address customer needs better while maximizing margins on future launches. They can leverage data and analytics in two main areas.

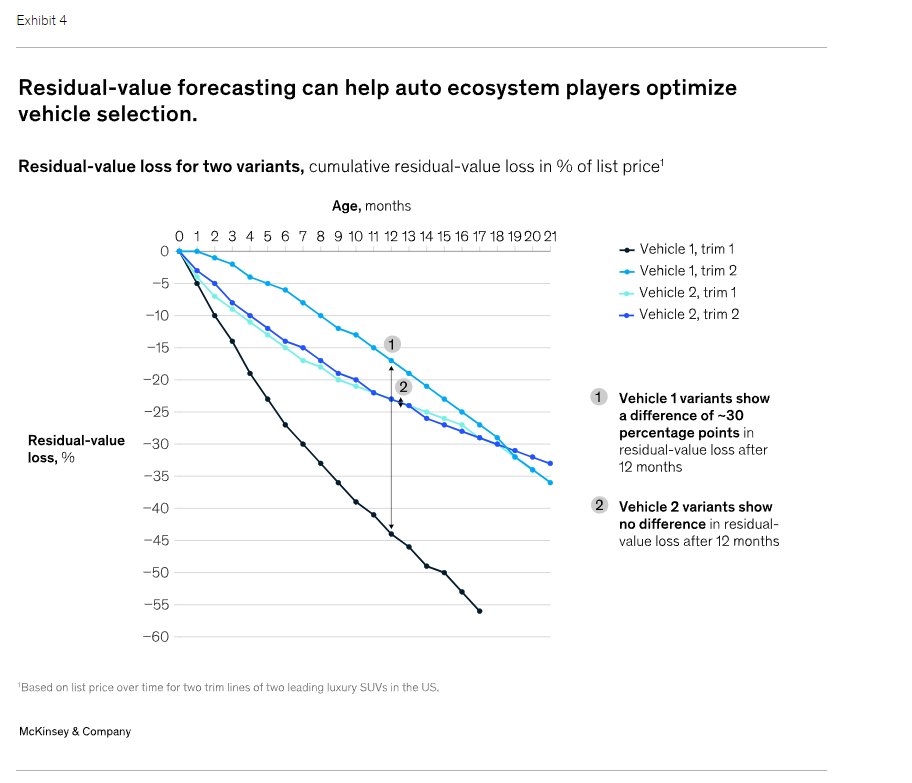

Product configurations and trim lines. Different trims and feature configurations can have vastly different rates of sale and residual-value decline. Analytics can help OEMs identify the highest-performing features within the vehicle category and incorporate them in future vehicle iterations. For instance, an analysis of recently produced midsize luxury SUVs in similar segments indicated that roughly 75 percent of them have roof rails and 60 percent have laser headlights. SUVs with these features also have better residual values in the long term. OEMs in this space could use this market data to add features that maximize long-term residual value of the trim line and improve vehicle desirability.

Wholesale pricing. Retail markups can differ significantly between dealers across geographies. Using data and analytics to understand retail pricing across the used-car markets can help OEMs define optimal wholesale prices for lease returns or trade-ins to maximize margins.

Auto finance companies

Understanding and optimizing the residual value will be critical for the global auto-finance sector2—and even more so with increasing EV adoption. However, macroeconomic changes, technology disruptions, a more competitive OEM landscape, and regulation all make forecasting residual values extremely complex. What’s more, rising interest rates will increase the cost of financing and push auto finance companies to choose between maximizing margins and maximizing volume. Our assessment suggests that residual-value optimization could present a $20 billion margin opportunity for auto finance companies across the United States and Europe. Auto finance companies can leverage data and analytics in two ways.

Choosing the right car. Leasing companies and banks can leverage historical used-car data to understand residual values across trim lines and models. Companies could then select the optimal combination based on local demand. As such, companies can select trims that they could add to their vehicle park to maximize residual value at the end of contracts.

Configurations and contract length for leased vehicles. Residual-value stability can vary greatly between different configurations of the same model of vehicle. Banks and leasing companies can determine the trims and equipment configurations of a given model with the highest residual-value stability. This data can also help them identify the optimal contract length for each vehicle, minimize the rate of value loss during the lease period, and determine the best lease rate for each vehicle. Furthermore, real-time analyses of residual-value risk can help companies minimize exposure by offering a dynamic contract renewal at the inflection point.

For example, Exhibit 4 shows differences in residual-value loss between two similar variants of two vehicles. Banks and leasing companies can use this comparison to recommend trim one for vehicle one instead of trim two—because trim two will lose more value at the end of the lease.

Companies leveraging data and analytics in the used-car market could capture their potential value across the ecosystem. Insights gleaned from advanced data and analytics can help companies make better decisions to increase margin potential, satisfy customer expectations, and improve sales performance. Companies can also leverage recent developments, such as generative AI, to build use cases that help spread awareness, encourage adoption, and improve education, even if these technologies are not required to capture value. As external factors influence the market, staying abreast of these options will be key to remaining competitive.

—

This article first appeared on www.mckinsey.com

Seeking to build and grow your brand using the force of consumer insight, strategic foresight, creative disruption and technology prowess? Talk to us at +971 50 6254340 or engage@groupisd.com or visit www.groupisd.com/story